In the race toward a cleaner, circular future, the top waste-to-energy companies to watch in 2025 will define who succeeds in turning trash into power. Inside this article, we profile 20 pioneering firms ranging from global incumbents to agile waste-to-energy startups that are deploying next-gen waste-to-energy technologies and scaling real projects.

By 2025, momentum is building: governments are tightening emissions rules, capital is shifting toward carbon avoidance, and cities are desperate for landfill alternatives. The banner of energy from waste companies no longer applies just to incinerators—today’s leaders are integrating advanced gasification, chemical recycling, and anaerobic digestion (AD). These hybrid approaches aim to squeeze more value from waste, reduce CO₂ footprints, and close material loops.

Among the key takeaways, a new generation of waste-to-energy companies is redefining how carbon is managed and reused. Established corporates such as Veolia and SUEZ are pairing traditional incineration systems with carbon capture pilots, effectively testing the frontier of negative emissions and turning what was once a pollutant into a recoverable resource.

Meanwhile, innovative waste-to-energy startups like Brightmark and LanzaTech are advancing the boundaries of chemical recycling and syngas fermentation, transforming discarded plastics and captured CO₂ into valuable fuels and industrial chemicals. At the same time, the biological side of the sector is scaling rapidly: anaerobic digestion (AD) plants that process food waste and organic fractions are being upgraded to produce renewable natural gas (RNG) and bio-fertilizer simultaneously.

Together, these developments illustrate a clear trend waste-to-energy technologies are evolving from simple disposal mechanisms into integrated, circular systems that recover energy, materials, and carbon in a closed loop.

2025 is pivotal because critical project pipelines mature, regulatory engines kick in, and visibility breeds momentum. The coming year could separate modular innovators from legacy operators. Through WtE case studies, Earth5R real-world municipal pilots offer early proof points. As you read on, each profile connects theory to practice—linking technology, finance, and impact. Let’s dive into the companies shaping tomorrow’s waste-to-energy horizon.

Why Waste-to-Energy Matters in 2025

Cities globally produce over 2.4 billion tonnes of municipal solid waste each year, and much of it still goes to open dumps or inefficient landfills. With methane emissions from landfills (a potent greenhouse gas) under scrutiny, the value of waste-to-energy technologies becomes increasingly central to climate policy.

Governments in Europe, China, India, and North America are pushing circular economy mandates and landfill bans that drive demand for advanced technology. Without innovation, many legacy incinerators will struggle to meet future emissions rules. That’s where the hybrid strategies of 2025 ;incineration and capture, or gasification and syngas valorization-get real.

This article’s methodology relies on public filings, company disclosures, industry reports, and WtE case studies Earth5R, which show the value of upstream waste management in improving plant feedstock quality and system resilience.

20 Waste-to-Energy Companies to Watch in 2025

Veolia:Turning Global Waste into Power: Veolia’s Carbon-Smart Energy Revolution

Veolia is one of the most versatile and large-scale players among energy from waste companies, deploying incineration, anaerobic digestion (AD), landfill-gas recovery, biomass, and fuel blending across its global operations. In a typical year, it processes over 14 million tonnes of landfill waste to generate ~1.2 million MWh of electricity via its gas capture systems. Beyond landfills, Veolia operates “more than 90 waste incineration power plants” worldwide, reducing waste volume to ~10% and recovering heat or electricity to supplement grids or district heating.

A striking example is the Istanbul WtE plant: Veolia operates a facility processing 1.1 million tonnes/year of non-recyclable municipal waste, paired with an 85 MW turbine that generates ~560,000 MWh annually, effectively avoiding ~1.5 million tonnes CO₂ emissions per year relative to landfill see here .That scale anchors Veolia’s position in our Top Waste-to-Energy Companies to Watch in 2025 list.

On innovation, Veolia recently rolled out its Drop® technology (incineration above 900 °C) to destroy PFAS (“forever chemicals”) with efficiency up to 99.9999%. That deployment spans 20 incineration lines across Europe see here. In hazardous waste, Veolia plans to expand capacity by 530,000 tonnes/year by 2030 via organic growth and tuck-in acquisitions. see here

On the AD and biogas side, Veolia also partners in biomethane unitsmfor instance, it and Waga Energy commissioned a new RNG unit at Granges Waste Recovery Center in France, its 6th such joint unit. see here In North America, Veolia is investing ~$300 million in upgrading its hazardous waste incinerator campus in Gum Springs, Arkansas, to handle 100,000 tons/year of hazardous waste. see here

Veolia’s breadth gives it a rare resilience. It can lean on large municipal incinerators, hedge with digestion and gas recovery, and push cutting-edge emissions tech and patents (notably PFAS destruction) to remain at the frontier of waste-to-energy technologies

Visit: Veolia: water, energy and waste recycling management services

SUEZ:From Waste to Hydrogen: How SUEZ is Powering the Future of Circular Energy

SUEZ occupies a unique position among energy from waste companies by blending incineration, heat & power recovery, hydrogen production, and CO₂ capture pilots within several of its facilities. In 2023 alone, SUEZ reported producing 7.7 TWh of energy from its waste and wastewater operations and avoiding 6.4 million tonnes of CO₂ equivalent through material recovery and energy conversion.see here

A flagship illustration is the Créteil energy-from-waste plant in the greater Paris region. Under a 20-year concession, SUEZ upgraded this plant to process 345,000 tonnes/year of mixed waste, converting it into green electricity, heat for district heating, and hydrogen for local fleets. The facility also integrates greenhouses heated by waste heat to grow tomatoes-an example of circular synergies.see here Moreover, SUEZ plans to build a hydrogen production & distribution unit linked directly to the WtE plant, expected to avoid ~1,500 tonnes CO₂/yr in its first phase.

On the carbon capture front, SUEZ is actively developing two CCS projects in the UK’s East Coast Cluster at its Teesside (Haverton Hill) and Wilton plants. These projects target capturing up to 900,000 tonnes CO₂ annually, with transport to North Sea aquifers for storage, in partnership with Technip Energies and Fluor.see here Meanwhile, at its Terres d’Aquitaine site in France, SUEZ has launched a biogenic CO₂ recovery unit, which captures 3,500 tonnes of CO₂ per year from anaerobic digestion, cleans it, and supplies it to greenhouse operations locally.see here

Because SUEZ is deploying hybrid systems—incineration and CO₂ capture, hydrogen co-production, AD integration,it sits at the frontier of waste-to-energy technologies. As policy regimes shift to penalize CO₂, and carbon credits reward capture, SUEZ’s ability to retrofit existing facilities rather than build new ones gives it an adaptable edge in the 2025 transition

Visit:SUEZ in India | Water Management Solutions

Covanta’s Energy-from-Waste Legacy: America’s Baseload Waste-Power Pioneer

Covanta is among the largest U.S.-based operators of energy-from-waste companies, executing municipal mass-burn incineration under long-term municipal contracts. Its fleet spans ~41 waste-to-energy plants in North America and Europe, processing approximately 21 million tons of waste annually and generating around 10 TWh of baseload electricity, while also recovering ~600,000 tons of metals.

One flagship example is the Covanta Onondaga plant in New York, which processes ~350,000 tons/year of municipal solid waste and produces ~220,000–225,000 MWh of electricity. Over its lifetime, it is credited with diverting ~4 million tons of CO₂ equivalents via landfill avoidance.see here Meanwhile, the Delaware Valley Resource Recovery Facility (Chester, PA) is among the U.S.’s largest which is designed to burn ~3,510 tons/day and produce up to ~90 MW net.

Covanta’s strength lies in scale, longevity, and contractual reliability. Analysts say that “for each ton of waste we recover for energy, Covanta saves 1 ton of CO₂ equivalent”—a rough but oft-cited heuristic used in EIA/industry reporting.see here. The company is currently expanding capacity: for instance, Pasco County, Florida approved a $550 million expansion to increase capacity from 1,050 to 1,565 tons/day.see here

Because Covanta offers proven economics in mature markets, it will likely remain a reference point in your Top Waste-to-Energy Companies to Watch in 2025 list. Its known performance and contract stability place it as a baseline against which riskier waste-to-energy startups or novel conversion pathways (gasification, pyrolysis) will be compared.

Enerkem’s Gasification Breakthrough: Converting Trash into Biofuels & Circular Chemicals

Enerkem is a poster child among waste-to-energy startups, specializing in converting non-recyclable municipal waste and biomass residues into biofuels and circular chemicals via gasification and catalytic synthesis. The company describes a strategic pipeline aiming to produce 1,000,000 tonnes/year of sustainable methanol across its portfolio.

Historically, Enerkem’s Edmonton facility served as a proof-of-concept: it processed ~40,000 tons of MSW/year and converted that into millions of litres of ethanol. Their gasification module uses pollution controls such as dual cyclones and a two-stage wet scrubber system to reduce particulates and acid gases.see here

In recent moves, Enerkem underwent financial restructuring to strengthen its backing and accelerate global growth, signaling confidence from investors in the circular chemicals and fuels path.see here The model is appealing: instead of burning syngas for heat, the platform aims to upgrade syngas to methanol or ethanol, capturing value in chemical markets rather than merely selling electricity.

One challenge, however, is scale: early plants handle lower throughput than typical incinerators, and supply chain consistency (feedstock variability, moisture, contamination) remains a risk. Still, in comparison with traditional WtE, Enerkem’s approach bridges the gap between waste-to-energy technologies and chemical recycling. In 2025, this hybrid philosophy could push it into broader adoption if capital and regulatory alignment are achieved.

Visit:https://enerkem.com/

Hitachi Zosen Inova (HZI) / Kanadevia Inova;Engineering the Future: HZI’s High-Efficiency Waste-to-Energy Plants Worldwide

Hitachi Zosen Inova (rebranded as Kanadevia Inova) is a leading global EPC and technology provider in the WtE space, delivering turnkey plants, retrofit services, and integrated options combining combustion, gas, and emissions control. As of 2024, HZI claims to have delivered over 600 reference projects since its founding (1933).see here

Its technology suite includes grate combustion, flue gas treatment, organic waste digestion (Kompogas®), and gas upgrading. HZI is also active in carbon capture pilots, such as its partnership with Enfinium to build the UK’s first modular CO₂ capture plant capable of capturing ~1 ton CO₂/day from a WtE facility.see here

In terms of flagship projects, HZI is constructing the Riverside 2 EfW plant for Cory in London, which is designed to accept ~650,000 tonnes/year of waste.see here Additionally, the company’s involvement in the Abu Dhabi ultra-large WtE contract (900,000 t/year) demonstrates its ambition in high-volume deployments.see here

Because HZI combines deployment, operations, retrofit, and innovation—including gasification, emissions control, and carbon capture—it serves as a backbone technology partner. In your Top Waste-to-Energy Companies to Watch in 2025, HZI’s role is often less front-end brand and more essential builder and integrator. Its modular CO₂ capture efforts and its deep project pipeline make it critical as policies shift toward emissions controls.

Visit: Hitachi Zosen Inova

Babcock & Wilcox (B&W);Reinventing Combustion: B&W’s Carbon-Capture-Ready WtE Systems

Babcock & Wilcox (B&W) brings established engineering heft to the WtE world, specializing in combustion systems, boiler design, feed systems, and emissions control modules. With over 155 years of engineering legacy, B&W’s WtE division designs and services major boiler and environmental systems.see here

One emblematic project is the Palm Beach Renewable Energy Facility (PBREF No. 2) in Florida. B&W engineered three mass-burn boilers and associated systems to process ~3,000 tons/day of municipal solid waste, delivering up to 95 MW gross, enough to power ~55,000 homes. see here. In Europe, B&W is developing the Kelvin WtE plant (UK), designed to divert 395,000 tonnes/yr and generate ~44 MW of energy.see here

On the forward-looking side, B&W has been awarded a FEED contract for Canada’s first WtE and CCS project (Varme Energy, Alberta), designing a waste-fired boiler, emissions systems, and post-combustion capture modules—expected capacity: ~200,000 tons/year. see here Furthermore, its collaboration in Greenland’s Nuuk & Sisimiut facilities showcases adaptability in extreme climates. see here

B&W is also a leader in retrofit upgrades: its SolveBright™ and OxyBright™ carbon capture technologies, plus integration of flue gas condensation energy recovery, aim to push older WtE fleets toward higher efficiency and lower emissions. In the context of Top Waste-to-Energy Companies to Watch in 2025, B&W’s role is essential: it doesn’t always own plants, but its engineering, innovation, and emission-reduction systems will determine whether legacy facilities survive the net-zero transition.

Mitsubishi Heavy Industries (MHI);MHI’s Advanced Waste Conversion: Stokers, Gasifiers, and Ash-Melting Mastery

Mitsubishi Heavy Industries (MHI) is a heavyweight OEM that supplies stoker furnaces, gasification modules, ash-melting systems, and full plant equipment to municipal and industrial WtE projects. Its MSW gasification & ash-melting line is typically offered in modular units (e.g., 120 t/d × 2 → 240 t/d, ~4.6 MW electrical demonstration) and has been used in retrofit and greenfield plants across Japan and Asia. These systems are engineered for low dioxin emissions (reported stack dioxins down to 0.00011 ng-TEQ/Nm³ in some installations) and robust uptime, which matters to municipal clients that require continuous service. See here

Beyond hardware, MHI’s strength is integration: it refurbishes core equipment (fluidized-bed, stoker lines) to improve thermal efficiency and extend asset life-work that directly links to the retrofit strategies discussed in our [Comparative Technology Primer]. MHI’s projects (e.g., Kushiro plant refurbishment) typically target multi-year availability and incremental efficiency gains, which helps aging fleets meet new emission regimes.see here

Why watch: when cities seek low-risk modernization rather than replacement, MHI is the vendor governments and EPCs turn to. Its combination of combustion, gasification, and ash-melting expertise makes it a one-stop engineering partner for energy from waste companies planning upgrades or fuel diversification.

Visit: Mitsubishi Heavy Industries (MHI)

Kawasaki Heavy Industries;Hydrogen from Waste: Kawasaki’s Circular Power & Clean Fuel Vision

Kawasaki Heavy Industries plays a strategic role at the intersection of WtE and the hydrogen economy, supplying gasifiers, liquefaction/storage for hydrogen, and transport ships for liquefied hydrogen trade. While known worldwide for its hydrogen carriers and liquefaction technology, Kawasaki is also developing WtE-adjacent projects that integrate syngas upgrading and low-carbon hydrogen production, positioning the firm as a systems integrator rather than just an equipment vendor.

Reuters reporting and company statements show Kawasaki pursuing hydrogen supply chains and co-fired pilot projects as part of broader industrial decarbonization strategies. see here

Kawasaki’s value proposition for WtE stakeholders is twofold: first, its hydrogen logistics and liquefaction know-how enable novel downstream uses for waste-derived syngas (for example, hydrogen synthesis from gasified residues); second, the firm’s maritime assets can link regional hydrogen hubs to markets, an advantage for large utilities and industrial clusters seeking cross-sector decarbonization. The company’s pivot to hydrogen supply chains (including lessons from the Australia-Japan trial) underscores how WtE projects might feed into broader low-carbon fuel networks.

Why watch: Kawasaki’s portfolio could enable waste-to-energy technologies to plug directly into hydrogen and ammonia value chains, which is an important differentiator as 2025 policy favors sector coupling and industrial symbiosis.

Visit:Kawasaki Heavy Industries

Keppel Seghers;Tuas Transformation: How Keppel Seghers Is Reinventing Urban Waste-to-Energy in Asia

Keppel Seghers is a leading EPC and operator across Asia, notable for compact, high-efficiency WtE plants and mega-projects such as Singapore’s Tuas Integrated Waste Management Facility (IWMF) and the Tuas WtE Plant (800 t/d, ~22 MW). Keppel’s Tuas portfolio is part of a S$1.5 billion master plan. It combines incineration, material recovery, and sludge treatment to maximize land use and energy recovery in dense cities. Keppel Seghers’ solutions emphasize modularity, flue-gas treatment, and long-term O&M under PPP models, which is essential for urban jurisdictions balancing NIMBY concerns with limited land.see here

Operationally, Keppel’s plants often pair grate combustion with advanced flue-gas treatment supplied by specialist vendors, delivering compliance with stringent local standards while supplying heat and electricity to municipal grids. The Tuas IWMF concept (IWMF Phase 1 designed for thousands of t/d capacity in later phases) shows how Keppel packages multiple waste streams, such as incinerable waste, source-segregated food waste, and dewatered sludge, into a single integrated facility. This integrated approach reduces feedstock variability and improves lifecycle outcomes, a theme echoed in our [Case Studies & Evidence] section.

Why watch: Keppel Seghers is a model for dense urban solutions where land and resources are constrained; its IWMF work makes it a go-to contractor for cities seeking a single-partner integrated WtE solution.

Visit:Keppel Seghers

Valmet;Automation at the Core: Valmet’s Smart Control Systems for Next-Gen WtE Plants

Valmet’s role in the WtE sector is primarily as the plant “brain,” and it engages in automation, combustion optimization, and process analytics for grate, CFB, and SRF plants. Valmet DNA automation and Valmet’s visible thermal imaging & combustion manager solutions have been shown to raise grate throughput, reduce auxiliary fuel use, and improve uptime with measurable KPIs for plant economics. For example, Valmet supplied DNA automation to three WtE plants in Sungnam City, Korea, to centralize operations and boost efficiency and emissions performance. see here

On the technology side, Valmet also supplies CFB boilers, biomass gasifiers, and plant-wide energy solutions, enabling multi-fuel flexibility, which helps plants adapt to changing RDF or SRF feedstock. Its recent case work (e.g., optimization at MVV Ridham Dock and deployments of furnace imaging) illustrates how digital controls can deliver 3–6% improvements in net efficiency which is significant at utility scale. These operational gains directly impact lifecycle emissions and the financial case for retrofit vs new builds.see here

Why watch: Valmet is the operational multiplier; its automation can convert a mediocre plant into a high-performing asset, making it indispensable for operators and a key vendor among energy-from-waste companies seeking improved LCA performance.

Visit: Valmet: technologies, services and automation to pulp, energy and paper industries

AI Meets Incineration: EBARA’s Intelligent Waste-to-Energy Systems for Smarter Cities

EBARA is a veteran Japanese supplier of stoker-type incinerators, gasification systems, and digital operation tools; the company claims delivery of over 500 stoker-type units and active operation of 80+ facilities in Japan. EBARA’s recent focus has been on marrying mechanical reliability with IoT/AI for predictive maintenance ; automatic crane systems, waste identification AI, and robot inspection services to reduce downtime and improve feedstock handling. These upgrades matter in crowded urban settings where compact, reliable units are necessary.see here

EBARA also emphasizes low-residue operation and energy recovery in compact footprints; its tech is widely used for municipal and industrial waste in Asia. The company’s export of control-system know-how (e.g., Ebara Densan) supports international deployments where local partners require turnkey operation and remote monitoring. For feedstock-sensitive projects, EBARA’s digital suite reduces manual sorting costs and helps maintain combustion stability-factors highlighted in our Comparative Technology Primer. see here

Why watch: EBARA is the go-to supplier for space-constrained urban plants and markets that prize operational reliability; its push into AI/IoT also makes it a quietly influential player in improving plant LCA performance.

Visit: EBARA

Japanese Precision, Global Impact: JFE’s Advanced Gasification & Ash-Melting Solutions

JFE Engineering offers a broad portfolio-stoker incinerators, gasification & melting systems, ash melting furnaces, RDF production—and has a long history of delivering high-temperature melting systems (over 1,600°C) for hazardous and municipal wastes. Recent orders include modular WtE plants (e.g., 500 t/d–1,080 t/d projects) that supply 35 MW+ of power while providing heat for district networks; JFE’s “Hyper 21” stoker and gasification-melting systems are engineered for extremely low residuals and stable combustion. see here

Technically, JFE’s continuous slag tapping and plasma/ash-melting approaches reduce unburnt carbon and stabilize heavy metals in slag, improving residue management and lowering landfill risk. Its R&D papers outline strategies for low-excess-air combustion and heat recovery that raise plant R1 efficiency relevant to operators facing tighter EU and Japanese emission constraints. JFE’s turnkey capability from design to commissioning—makes it valued by municipalities seeking guaranteed performance. see here

Why watch: JFE blends advanced thermal engineering with practical EPC delivery, making it ideal for projects that must handle mixed or hazardous feedstocks while meeting strict residue and emission standards.

Visit: JFE Engineering

America’s Energy Recovery Backbone: Wheelabrator’s Proven WtE Operations

Wheelabrator is a major U.S. mass-burn operator with a long operational footprint—running many municipal WtE plants such as the iconic Wheelabrator Baltimore (≈64–65 MW net at Westport) and others across the northeastern U.S. Historically, Wheelabrator’s model centers on long-term municipal contracts, baseload generation, and metal recovery from ash streams. These steady cash flows and operational expertise make it an important comparator against newer waste-to-energy startups pursuing alternative conversion pathways.

However, Wheelabrator’s plants have faced community scrutiny and permit challenges around air emissions serving as an important cautionary tale about the social license required for WtE projects. Modernization and emissions-control retrofits (baghouse upgrades and SCR for NOx) are central to keeping these assets compliant and viable as policy tightens. In many policy settings, these incumbents form the baseline service that newer technologies must beat on LCOE and emissions performance.

Why watch: Wheelabrator remains a bellwether for municipal acceptance and regulatory resilience in mature markets; it illustrates the political and operational dimensions that any Top Waste-to-Energy Companies to Watch in 2025 must navigate.

China’s Green Giant: Everbright’s Scalable Model for Waste-to-Energy Growth

China Everbright Environment is a scale player in China’s rapid WtE buildout, operating dozens of projects ranging from county-level 500 t/d plants to mega projects handling 2,000–3,000 t/d (e.g., Hangzhou 3,000 t/d examples). The company emphasizes standardization, replicable plant designs, and integration of food-waste digestion at selected sites to maximize resource recovery and reduce residue. Everbright’s portfolio demonstrates how standardized engineering at scale can lower unit costs and accelerate urban service deployment.see here

Operational features in Everbright projects include advanced flue-gas treatment, high-speed turbines, and community engagement hubs that frame plants as education centers,thus,helping manage NIMBY concerns. Several of its plants have received national quality awards and AAA ratings for operational and environmental performance, reflecting adherence to China’s evolving emissions standards. For cities with very large throughput, Everbright’s model shows how volume and standardization translate into lower per-ton costs and faster rollout.

Why watch: Everbright is essential for understanding the global WtE market because China’s scale sets global supply and project benchmarks, if you are comparing unit economics or replication strategies in your Top Waste-to-Energy Companies to Watch in 2025 piece, Everbright’s playbook is often the reference case.

Brightmark’s Plastic-to-Fuel Ambition: Circular Energy from Pyrolysis Innovation

Brightmark positioned itself as a commercial leader in chemical recycling, building large pyrolysis “circularity centers” designed to process up to 100,000 tonnes/year of mixed plastics into naphtha, diesel, and wax.

The Ashley, Indiana, facility was the flagship: announced as a 100,000 t/yr plant and intended to prove plastics-to-fuel at scale, the site sold its first pyrolysis oil in 2023. Brightmark also piloted RNG projects and planned regional feedstock hubs to integrate waste collection with downstream fuel markets.

Yet commercial scale-up in chemical recycling has been uneven. By 2025 Brightmark entered restructuring and bankruptcy processes, and coverage shows Ashley had operated at low utilization before being retained through sale processes an important caution on the economics of pyrolysis at scale. This financial turbulence underscores an industry lesson in our Comparative Technology Primer: pyrolysis can deliver circular feedstocks, but only if continuous, clean feedstock streams, robust offtake agreements, and supportive policy (EPR, recycled content mandates) are in place. see here

Why watch: Brightmark’s technology and project blueprint remain relevant because pyrolysis capacity is expected to expand worldwide; monitoring its commercial outcomes will signal whether plastics-to-fuel can move from demonstration to bankable utility. (\

Visit: Brightmark

From Carbon to Fuel: LanzaTech’s Bio-Fermentation Pathway to Sustainable Aviation Fuel

LanzaTech’s platform combines gasification and biology, capturing CO-rich syngas and fermenting it with proprietary microbes to produce ethanol and higher-value chemicals. The company’s technology underpins the CirculAir™ initiative with LanzaJet, which converts waste-derived ethanol into sustainable aviation fuel (SAF).

The Freedom Pines/LanzaJet Freedom Pines fuels site in Georgia is a milestone commercial plant producing ~10 million gallons/year of SAF from alcohol-to-jet processing fed by low-carbon ethanol streams—showing how gas fermentation can feed established fuel value chains. see here

LanzaTech has evolved through strategic partnerships and equity moves; after scaling fermentation pilots, the platform attracted industrial off-takers and integrators seeking to decarbonize hard-to-abate sectors like aviation.

Key advantages of the approach include high carbon-utilization efficiency (converting carbon in syngas to liquid fuels) and flexibility to accept multiple syngas sources, including gasified MSW or industrial off-gas streams. Still, success depends on upstream gasifier reliability and syngas cleanup, technical links highlighted in our Comparative Technology Primer.see here

Why watch: LanzaTech and its partnership with LanzaJet point to a commercially viable pathway where waste-to-energy technologies feed into global SAF and chemicals markets, making it one of the more mature waste-to-energy startups to follow in 2025.

Visit:LanzaTech’s

Inside Agilyx: Depolymerizing Plastic Waste into Circular Chemical Feedstocks

Agilyx focuses on depolymerization technologies,particularly polystyrene and mixed plastics—to recover monomers and circular feedstocks rather than burning for energy. Historically it operated the Regenyx/Tigard chemical-recycling facility, a high-profile demonstration of polystyrene depolymerization and feedstock recovery.

However, in 2024–2025, Agilyx faced financial and operational headwinds: the Tigard plant closed in 2024, and broader industry audits have questioned environmental and economic performance for some chemical-recycling pilots.

Agilyx’s technical value lies in targeted depolymerization when feedstock is appropriate (e.g., relatively pure polystyrene), depolymerization can yield high-value monomers and reduce virgin polymer demand. The company continues to license its Styrenyx™ process and pursue partnerships to place modular depolymerization units near feedstock sources.

But the firm’s recent operational setbacks illustrate the capital-intensity and feedstock-quality challenges that the chemical-recycling segment faces ,points explored in this article’s Comparative Technology Primer and Case Studies & Evidence sections.see here

Why watch: Agilyx’s technological niche, if paired with stable feedstock supplies and off-takers, could become an important complement to incineration and gasification for specific polymer streams; its near-term trajectory will indicate whether depolymerization is scalable and bankable

Visit: Agilyx

AI Sorting for a Cleaner Feedstock: How AMP Robotics Is Powering Smart Waste Streams

AMP Robotics is widely recognized as the upstream multiplier for waste-to-energy technologies: its AI-driven robotic sorters and the AMP Cortex platform improve feedstock quality by extracting recyclables and contaminants, producing higher-grade RDF/SRF for downstream combustion or chemical processes.

Recent deployments include a fully integrated AI facility processing ~62,000 tonnes/year of single-stream recycling and multiple MRF integrations that report contamination reductions of 30–50%, faster throughput, and better commodity yields.see here

Operationally, AMP’s systems use computer vision and machine learning to identify and pick flexible plastics, cartons, and other valuable fractions that conventional screens miss. For WtE plants, better upstream sorting reduces ash content, improves calorific value, and lowers emissions,making AMP a strategic partner to both energy-from-waste companies and chemical-recycling pilots.

The company also highlights data-driven performance monitoring, enabling MRF operators to optimize routes, staffing, and equipment investment decisions.see here

Why watch: As regulators and buyers demand cleaner material streams, AMP’s technology reduces feedstock variability, directly improving lifecycle metrics and the economics of WtE projects; it is therefore essential to track as part of any WtE deployment strategy

Visit: AMP Robotics

Plasma Power: PyroGenesis’ High-Temperature Solution to Complex Waste Challenges

PyroGenesis (Pyrogenesis) specializes in high-temperature plasma gasification, a thermal technology designed to safely treat complex and hazardous wastes (PFAS-contaminated materials, industrial sludges) and produce syngas with minimal residuals.

Recent field evidence shows PyroGenesis’ plasma torches have successfully destroyed PFAS-contaminated material and treated hundreds of tonnes in pilot campaigns, while reducing energy requirements versus legacy thermal routes.

The company has reported contracts and milestone payments tied to PFAS remediation projects and demo plants.see here

The technical advantage of plasma is its ability to reach extreme temperatures (>5,000 °C) that break down persistent organics and immobilize metals in a vitrified slag useful for hazardous or mixed industrial streams that traditional incineration cannot process safely.

Economically, plasma systems are capital-intensive, but they offer unique value for high-risk feedstocks and remediation contracts, complementing mass-burn WtE and chemical recycling in a full portfolio approach. Pilot results demonstrate low residue and high destruction efficiencies, positioning PyroGenesis as a specialized partner for niche waste streams. see here

Why watch: PyroGenesis is a strategic player when cities or industries need PFAS destruction or treatment of legacy contaminated materials,capabilities that will likely be in demand as regulators tighten controls on persistent pollutants

Visit: PyroGenesis

Europe’s Integrated Circular Leader: How Indaver Is Redefining Waste Recovery and Energy

Indaver is a European full-service operator focused on integrated resource recovery: combining materials recycling, incineration and energy recovery with strict residue management.

Its Meath WtE facility (Ireland) processes ~200,000 tonnes/year of residual municipal waste and generates ~18–21 MW of electricity (~110 GWh/yr), powering tens of thousands of homes. Indaver’s footprint in Europe handles millions of tonnes annually. its 2024 sustainability report indicates ~4.6 million tonnes were processed in its own installations.

Indaver’s strength is systems integration and regulatory compliance: its plants are designed to meet tight EU emission standards while maximizing landfill diversion and material recovery.

Projects such as Rivenhall (UK) and Meath illustrate how an operator can combine recycling, energy export, and community engagement to secure social license and economic viability. Indaver also invests in LCA-driven performance reporting and community transparency practices that improve the public case for WtE deployment. see here

Why watch: Indaver is a model of the European integrated approach—if policymakers favor centralized, tightly regulated recovery hubs, Indaver’s business model will likely be central to urban waste strategies and to any Top Waste-to-Energy Companies to Watch in 2025 list focused on compliant, scalable systems.

Visit: indaver.com

From Landfill to Light: Real Projects Powering the Waste-to-Energy Revolution

Case Study 1; Earth5R : urban city waste projects

In India, Earth5R has emerged as a practitioner-researcher, deploying citizen-centric waste models with measurable impact. In Indore, for example, the municipal corporation adopted a comprehensive system of door-to-door collection, six-stream waste segregation, and integration of composting and recycling, in coordination with Earth5R’s community modeling.

Over time, Indore achieved 100 % source segregation and cut dumping to open landfills helping it win “cleanest city” recognition several years in a row.see here

Earth5R’s “End-to-End Urban Waste Management Blueprint” now serves as a replicable framework: it emphasizes waste flow monitoring, app-based carbon tracking, data transparency, and public-private governance collaboration. see here

These projects, though not full WtE facilities themselves, provide bottom-up evidence that improved upstream waste control boosts feedstock consistency and lowers processing residues critical in real plant economics (see Comparative technology primer).

Case Study 2; Project-level evidence: Enerkem Edmonton, Indaver Meath & more

Enerkem’s Edmonton waste-to-biofuels facility is often cited as a benchmark. It processed up to 40,000 tonnes per year of non-recyclable municipal solid waste and produced about 5 million litres of biofuels, operating over 15,000 hours before decommissioning.see here

According to U.S. regulatory filings, the facility diverted over 100,000 metric tonnes from landfills annually. In life-cycle terms, Enerkem reports emissions reductions exceeding 65 % compared to competing processes.see here

In Ireland, Indaver’s Meath plant processes ~200,000 tonnes of residual waste per year, generating around 18–21 MW of net electricity (~110 GWh/yr) which is enough power for some 20,000 households. Its integrated resource recovery model merges materials recycling, energy conversion, and highly controlled emissions, exemplifying how corporates can align with the waste-to-energy technologies roadmap.

Meanwhile, in Europe and the U.S., SUEZ’s upgraded Créteil WtE facility is undergoing retrofits to increase electrical efficiency, reduce flue gas losses, and pilot CO₂ capture systems (data subject to public release). Because such retrofits are central to many profiles in our Top Waste-to-Energy Companies to Watch in 2025, these real projects ground theory in practice.

Together, these case studies confirm that waste-to-energy is not a theoretical promise but a deployable suite of technologies: the upstream city systems like Earth5R strengthen feedstocks, while plants like Edmonton and Meath validate the conversion and emissions claims that underpin your article.

Comparative technology primer: How each technology work?

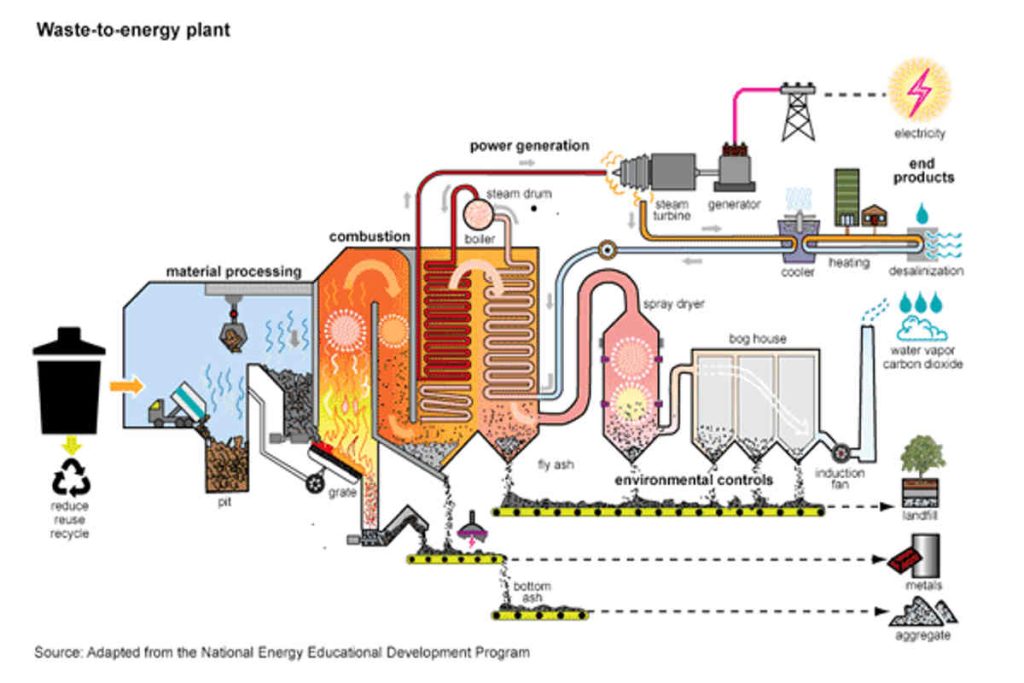

In the evolving landscape of waste-to-energy technologies, four pathways dominate conversations: incineration, gasification, pyrolysis, and anaerobic digestion (AD). In a modern mass-burn incinerator, waste is combusted at 800–1,000 °C under excess air; the heat raises steam for a Rankine cycle, often co-producing heat (CHP). Typical net electrical efficiencies for well-designed plants range 20–28 %.

In contrast, gasification operates under substoichiometric or partial oxidation conditions to convert waste into syngas (CO, H₂, CO₂), which can feed internal combustion engines or turbines. Combined cycle gasification plants may boost electrical efficiency into the 30–35 % range or higher under ideal conditions. (Theoretical studies show syngas cleaning reduces emission loads compared to straight combustion.)see here

Pyrolysis, meanwhile, thermally decomposes waste in the absence (or near-absence) of oxygen into char, oils, and syngas. Its strength lies in feedstock flexibility and modular scale, though energy efficiency often lags incineration without tight integration.

Anaerobic digestion is non-thermal: organic waste (food, sludge, yard waste) is biologically converted by microbes in sealed reactors to produce biogas (≈ 50–65 % methane + CO₂) plus digestate. Energy yields vary by substrate but a well-run digester might deliver 0.35–0.6 m³ CH₄ per kg volatile solids, translating to ~2–6 kWh electricity equivalent per kg of organics.

Thus, incineration is analogous to a large thermal engine, gasification is a refined intermediate fuel factory, pyrolysis is a modular “chemical cracker,” and AD is a biological fermenter converting softness (organics) into energy.

Emissions & lifecycle tradeoffs

When evaluating WtE lifecycle assessment, the tradeoff between methane avoided from landfills and CO₂ emissions from combustion looms large. Landfills emit methane ; a potent greenhouse gas (about 25–82× stronger than CO₂ over 20 years) and many see here landfills fail to capture all of it. Recent satellite analyses of U.S. urban landfills suggest actual collection efficiencies average ~38%, far below the 70 % often assumed in inventories.see here

In a comparative LCA of incineration vs. gasification, for 1 kWh of electricity produced, one study found that incineration emits on average 200–400 g CO₂-eq (net), depending on energy credits and landfill diversion assumptions. see here

Meanwhile, gasification with syngas cleanup tends to produce lower overall burdens in human health and environmental impact categories, thanks to less flue gas emissions and more efficient energy conversion.see here

AD, on the other hand, often records negative net CO₂ in LCAs when substituting for fossil natural gas because biogenic methane displaces fossil fuel consumption—but only when feedstock is fresh organic.

The constraint is that AD handles only the biodegradable fraction and not plastics or residuals. In contrast, pyrolysis systems often show intermediate emissions and energy profiles; they can reduce environmental load if char and syngas are fully valorized, but poor conversion or gas cleaning may erode gains.

FAQs on Top Waste-to-Energy Companies to Watch in 2025

What is driving the global rise of waste-to-energy technologies in 2025, and how do they fit into broader climate goals?

The growth is driven by stricter landfill bans, carbon pricing, and circular economy targets. Waste-to-energy technologies reduce methane from landfills while generating clean power and renewable fuels.

How does the Top Waste-to-Energy Companies to Watch in 2025 list reflect market change?

It highlights a shift from traditional incineration to integrated systems combining energy recovery, carbon capture, and chemical recycling across major regions.

Which companies are leading in carbon capture integration?

Veolia and SUEZ lead with incineration-plus-carbon-capture pilots in Europe, testing negative-emission models at operational plants.

How do incineration, gasification, pyrolysis, and AD differ?

Incineration burns waste for heat; gasification converts it into syngas; pyrolysis turns plastics into oils and gases; AD uses microbes to make biogas from organics.

How do lifecycle assessments balance landfill methane against CO₂ emissions?

LCAs show WtE can cut net emissions by avoiding landfill methane leaks, even when accounting for combustion CO₂ output.

Why are startups like Brightmark and LanzaTech important?

They’re pioneering chemical recycling and carbon fermentation, converting plastic and CO₂ waste into fuels and feedstocks.

What lessons do Earth5R’s city projects teach?

They prove that community-led segregation and traceable waste systems improve feedstock quality and plant efficiency downstream.

How does Enerkem’s gasification process perform compared to incineration?

Enerkem’s plants transform non-recyclable waste into low-carbon methanol and biofuels, reducing emissions by up to 65%.

Why is Indaver’s Meath plant a benchmark?

It integrates recycling, energy recovery, and residue management, powering over 20,000 homes while meeting EU emission standards.

What role do HZI and JFE Engineering play in modernization?

They provide EPC and turnkey WtE solutions, retrofitting existing plants and building advanced low-emission facilities globally.

How are Valmet and AMP Robotics improving operations?

Their AI and automation tools boost combustion control, uptime, and feedstock purity, cutting emissions and maintenance costs.

Why is China Everbright Environment significant for emerging markets?

It demonstrates scalable, standardized WtE design, rapidly deploying high-efficiency plants in fast-growing Asian cities.

How do MHI and Kawasaki link WtE to hydrogen?

They integrate gasification with hydrogen and ammonia production, creating pathways for waste-derived clean fuel.

What makes Babcock & Wilcox’s retrofits important?

Their carbon-capture and boiler-upgrade systems extend plant life and reduce NOx and CO₂ footprints in older facilities.

What challenges did Brightmark and Agilyx face?

Both struggled with feedstock purity, financing, and scaling costs—key barriers to commercial chemical recycling viability.

How does LanzaTech’s technology work?

It ferments syngas into ethanol and SAF precursors, using captured carbon as feedstock for clean fuels and chemicals.

Which 2025 policies are boosting WtE investment?

Landfill bans, renewable fuel mandates, and carbon pricing are driving funding toward low-emission WtE projects.

How can companies get featured or linked in such articles?

They can share verified project data, LCA results, and request backlinks or interviews through transparent outreach.

How are companies like Indaver and Everbright gaining public trust?

They emphasize emissions transparency, community education centers, and local job creation around their WtE sites.

What should readers monitor through 2025?

Track verified emissions data, carbon-capture adoption, and lifecycle efficiency improvements among leading WtE firms.

Clean Energy Transition Through Waste-to-Energy Innovation

The next decade will belong to innovators who transform waste into opportunity. The companies highlighted in Top Waste-to-Energy Companies to Watch in 2025 prove that clean energy and circular resource recovery are not futuristic goals ; they’re happening now.

If you’re a policymaker, researcher, or sustainability leader, this is the time to act. Support projects that close the loop, invest in cleaner conversion technologies, and help cities adopt smarter waste-to-energy solutions. Every partnership, policy shift, or pilot plant brings the world one step closer to net-zero waste and carbon neutrality.

For startups and corporates, take inspiration from the frontrunners driving breakthroughs in gasification, carbon capture, AI-driven sorting, and chemical recycling. Collaborate, innovate, and share your data to strengthen the credibility and impact of the global waste-to-energy ecosystem.

The transition is already in motion be sure to be part of the movement that turns waste into a sustainable energy future.

Authored by- Sneha Reji